Formal compliance and substantial compliance: an ethical approach to quality management systems in Colombian audit firms

DOI:

https://doi.org/10.24142/rvc.n33a5Keywords:

professional ethics, quality management, substancial compliance, auditing, public trustAbstract

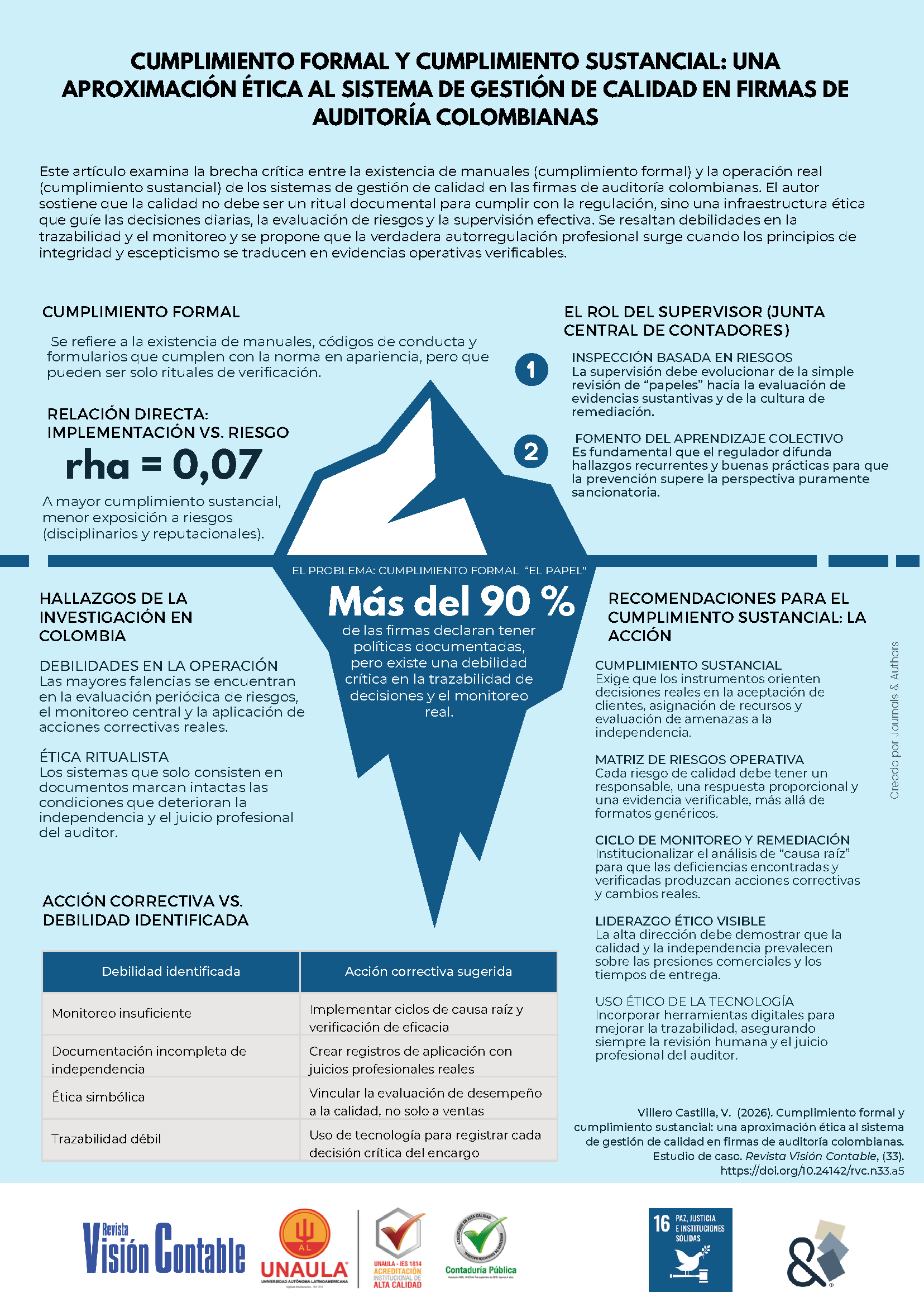

This article analyzes the gap between formal compliance and substantial compliance in quality systems implemented by Colombian audit firms from an ethical, organizational, and regulatory perspective. Using a mixed-method, descriptive-correlational, and cross-sectional design, the study integrates surveys, interviews, a focus group, and documentary review applied to auditors, partners, and quality leaders. Findings show progress in documentary formalization and declared ethical culture; however, weaknesses in risk assessment, monitoring, traceability, and remediation persist. The article concludes that audit quality cannot be reduced to manuals or checklists: it requires operational evidence, ethical leadership, and risk-based supervision. Recommendations are made to strengthen professional self-regulation, the preventive role of the Colombian Board of Accountants, and the public trust.

Downloads

References

Congreso de la República de Colombia. (1990). Ley 43 de 1990. Bogotá: Diario Oficial de Colombia núm. 39 602. Recuperado de https://www.funcionpublica.gov.co/eva/gestornormativo/norma.php?i=66148

Congreso de la República de Colombia. (2009). Ley 1314 de 2009. Bogotá: Diario Oficial de Colombia núm. 47 409. Recuperado de https://www.funcionpublica.gov.co/eva/gestornormativo/norma.php?i=36833

Consejo Técnico de la Contaduría Pública. (2025). Concepto 0136 de 2025: implementación de la NIGC 1. Recuperado de https://cijuf.org.co/sites/cijuf.org.co/files/normatividad/2025/CONCEPTO%200136.pdf

Creswell, J. W. y Plano Clark, V. L. (2017). Designing and conducting mixed methods research. Thousand Oaks (United States): SAGE.

DeAngelo, L. E. (1981). Auditor size and audit quality. Journal of Accounting and Economics, 3(3), 183-199. https://doi.org/10.1016/0165-4101(81)90002-1

DeFond, M. y Zhang, J. (2014). A review of archival auditing research. Journal of Accounting and Economics, 58(2-3), 275-326. https://doi.org/10.1016/j.jacceco.2014.09.002

Deming, W. E. (1986). Out of the crisis. Massachusetts (United States) Massachusetts Institute of Technology, Center for Advanced Engineering Study.

Francis, J. R. (2011). A framework for understanding and researching audit quality. Auditing: A Journal of Practice & Theory, 30(2), 125-152. https://doi.org/10.2308/ajpt-50006

Hernández-Sampieri, R. y Mendoza, C. P. (2018). Metodología de la investigación: las rutas cuantitativa, cualitativa y mixta. Ciudad de México (México): McGraw-Hill Education.

International Auditing and Assurance Standards Board – IAASB. (2020a). International Standard on Quality Management 1: Quality management for firms that perform audits or reviews of financial statements, or other assurance or related services engagements. IAASB. Recuperado de https://www.ifac.org/system/files/publications/files/IAASB-Quality-Management-ISQM-1-Quality-Management-for-Firms.pdf

International Auditing and Assurance Standards Board – IAASB. (2020b). International Standard on Quality Management 2: Engagement quality reviews. IAASB. Recuperado de https://www.ifac.org/system/files/publications/files/IAASB-Quality-Management-ISQM-2-Engagement-Quality-Reviews.pdf

International Auditing and Assurance Standards Board – IAASB. (2020c). International Standard on Auditing 220 (Revised): Quality management for an audit of financial statements. IAASB. Recuperado de https://www.ifac.org/system/files/publications/files/IAASB-International-Standard-Auditing-220-Revised.pdf

International Ethics Standards Board for Accountants – IESBA. (2023). Handbook of the International Code of Ethics for Professional Accountants, including International Independence Standards: 2023 edition. International Federation of Accountants. IESBA. Recuperado de https://ifacweb.blob.core.windows.net/publicfiles/2023-09/2023%20IESBA%20Handbook%20Final.pdf

International Forum of Independent Audit Regulators – IFIAR. (2026). Survey of inspection findings 2025. IFIAR. Recuperado de https://www.fsa.go.jp/ifiar/2025SurveyReport.pdf

Junta Central de Contadores. (2024). ¿Qué es inspección y vigilancia? JCC. Recuperado de https://www.jcc.gov.co/junta-central-de-contadores/organizaci%C3%B3n-de-la-uae---jcc/objetivos-estrategicos/qu%C3%A9-es-inspecci%C3%B3n-y-vigilancia

Juran, J. M. (1988). Juran on planning for quality. New York (United States): Free Press.

Kish-Gephart, J. J.; Harrison, D. A. y Treviño, L. K. (2010). Bad apples, bad cases, and bad barrels: Meta-analytic evidence about sources of unethical decisions at work. Journal of Applied Psychology, 95(1), 1-31. https://doi.org/10.1037/a0017103

Knechel, W. R.; Krishnan, G. V.; Pevzner, M.; Shefchik, L. B. y Velury, U. K. (2013). Audit quality: Insights from the academic literature. Auditing: A Journal of Practice & Theory, 32(Supplement 1), 385-421. https://doi.org/10.2308/ajpt-50350

Power, M. (1997). The audit society: Rituals of verification. Oxford (United Kingdom): Oxford University Press.

Presidencia de la República de Colombia. (2015). Decreto 2420 de 2015. Bogotá: Diario Oficial de Colombia núm. 49 726. Recuperado de https://www.funcionpublica.gov.co/eva/gestornormativo/norma.php?i=76745

Presidencia de la República de Colombia. (2026). Proyecto de decreto: Por el cual se modifica, actualiza y compila el marco técnico de las Normas de Aseguramiento de la Información del Decreto 2420 de 2015. Recuperado de https://www.mincit.gov.co/normatividad/proyectos-de-normatividad/proyectos-de-decreto-2026/19-03-2026-pd-nai-actualizado.aspx

Suddaby, R.; Gendron, Y. y Lam, H. (2009). The organizational context of professionalism in accounting. Accounting, Organizations and Society, 34(3-4), 409-427. https://doi.org/10.1016/j.aos.2009.01.007

Treviño, L. K.; Weaver, G. R.; Gibson, D. G. y Toffler, B. L. (1999). Managing ethics and legal compliance: What works and what hurts. California Management Review, 41(2), 131-151. https://doi.org/10.2307/41165990

Treviño, L. K., Weaver, G. R. y Reynolds, S. J. (2006). Behavioral ethics in organizations: A review. Journal of Management, 32(6), 951-990. https://doi.org/10.1177/0149206306294258

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Revista Visión Contable

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

Aquellos autores/as que tengan publicaciones con esta revista, aceptan los términos siguientes:- Los autores/as conservarán sus derechos de autor y garantizarán a la revista el derecho de primera publicación de su obra, el cuál estará simultáneamente sujeto a la Licencia de reconocimiento de Creative Commons que permite a terceros compartir la obra siempre que se indique su autor y su primera publicación esta revista.

- Los autores/as podrán adoptar otros acuerdos de licencia no exclusiva de distribución de la versión de la obra publicada (p. ej.: depositarla en un archivo telemático institucional o publicarla en un volumen monográfico) siempre que se indique la publicación inicial en esta revista.

- Se permite y recomienda a los autores/as difundir su obra a través de Internet (p. ej.: en archivos telemáticos institucionales o en su página web) una vez sea publicado el artículo en la revista, lo cual puede producir intercambios interesantes y aumentar las citas de la obra publicada.